Page 75 -

P. 75

Notes to the Consolidated Financial Statements

31st March 2017

3 FINANCIAL RISK MANAGEMENT (CONTINUED)

3.2 Capital risk management (Continued)

The Group monitors capital on the basis of the gearing ratio. This ratio is calculated as total

borrowings net of cash and cash equivalents divided by total equity as shown in the consolidated

balance sheet.

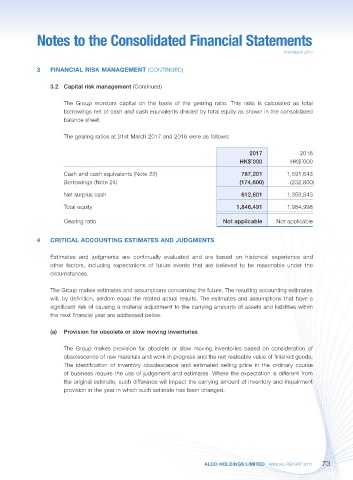

The gearing ratios at 31st March 2017 and 2016 were as follows:

2017 2016

HK$’000 HK$’000

Cash and cash equivalents (Note 22) 787,201 1,591,643

Borrowings (Note 24) (174,600) (232,800)

Net surplus cash 612,601 1,358,843

Total equity 1,846,491 1,984,998

Gearing ratio Not applicable Not applicable

4 CRITICAL ACCOUNTING ESTIMATES AND JUDGMENTS

Estimates and judgments are continually evaluated and are based on historical experience and

other factors, including expectations of future events that are believed to be reasonable under the

circumstances.

The Group makes estimates and assumptions concerning the future. The resulting accounting estimates

will, by definition, seldom equal the related actual results. The estimates and assumptions that have a

significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within

the next financial year are addressed below.

(a) Provision for obsolete or slow moving inventories

The Group makes provision for obsolete or slow moving inventories based on consideration of

obsolescence of raw materials and work in progress and the net realisable value of finished goods.

The identification of inventory obsolescence and estimated selling price in the ordinary course

of business require the use of judgement and estimates. Where the expectation is different from

the original estimate, such difference will impact the carrying amount of inventory and impairment

provision in the year in which such estimate has been changed.

ALCO HOLDINGS LIMITED ANNUAL REPORT 2017 73